The current Stamp Duty Land Tax (SDLT) holiday has helped deliver a property market stimulus that has far outweighed the immediate response to the 2007/08 financial crisis, according to new analysis by Search Acumen, the property data and insight provider.

Despite causing an uplift in activity, the current SDLT relaxation has so far triggered a 7% rise in house prices from June 2020 to February 2021, adding £17,265 to the price of the average home in England. This rise has more than offset the £2,572 SDLT savings made on the average property.

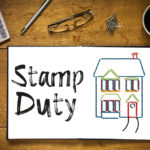

An average of 103,724 residential property transactions have occurred each month across England and Northern Ireland since the tax break was introduced in July 2020, up 22% from the 84,691 average in the 12 months to March 2020, before the first lockdown stalled the market.

Since the measure was introduced, 171,303 extra deals have taken place compared to the pre-Covid period in 2019/20.

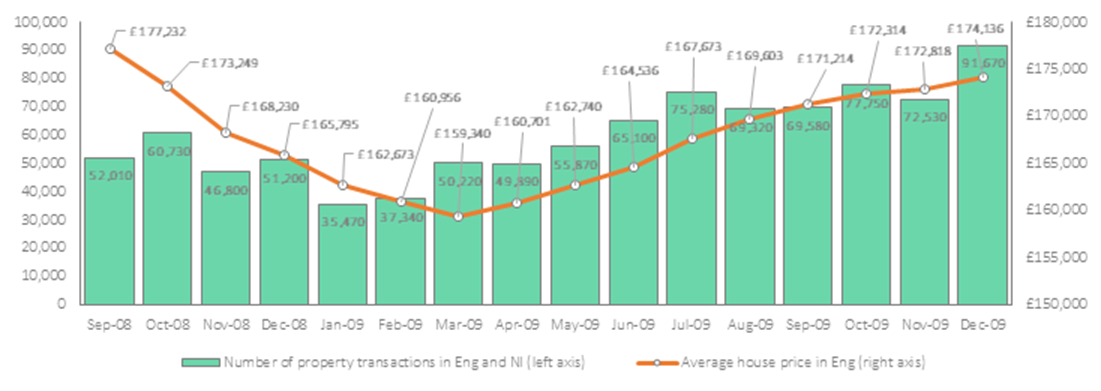

Search Acumen’s analysis shows the SDLT holiday of 2008/09 in the wake of the Great Financial Crisis saw an average of 60,048 transactions per month. This was down 27% from the previous 12-month average of 82,378 monthly residential property transactions.

Higher transaction volumes during the current holiday could be partly attributed to lending conditions being more favourable than in the aftermath of the financial crisis. Strong credit availability has helped property transactions progress despite pandemic-induced disruption to the economy, with the tightening of credit mainly concentrated in the high loan-to-value (LTV) segment of the mortgage market.

Prospective buyers have been able to access relatively cheap medium and low LTV mortgages to finance home purchases during the current SDLT holiday. In contrast, homebuyers suffered from lenders pulling back from the mortgage market during the Credit Crunch in 2008/09.

The impact on average property prices during the two SDLT holidays has also differed significantly. Since the current holiday was introduced, house prices in England have jumped 7% to £268,291 from £251,026. For comparison, the SDLT holiday of 2008/09 saw house prices in England fall 2% to £174,136 in December 2009 from £177,232 in August 2008.

Graph 1: Property transactions (Eng/NI) and average house prices (Eng) during the current 2020/21 SDLT holiday

Graph 2: Property transactions (Eng/NI) and average house prices (Eng) during the 2008/09 SDLT holiday

Andy Sommerville, Director at Search Acumen, says: “This analysis suggests the property market has been far more responsive to intervention compared to the post-financial crisis holiday.

“The housing market’s strong performance compared to the wider economy highlights the contrast between the current healthcare crisis and its economic impacts, and the 2008/09 crisis which was rooted in financial markets.

“While many households have absorbed income hits and face greater job insecurity, the UK’s financial system has held up reasonably well since the onset of Covid. Lenders did pull back from the mortgage market in the early stages of the pandemic, but the flow of credit has gradually picked up as banks got to grips with the crisis.

“As a result, financing for house purchases has been in reasonably good supply and worked in tandem with the SDLT holiday to generate a level of activity not seen for a decade, despite the unprecedented challenges of Covid-19. However, giving extra support for buyers has had many challenging consequences, from pushing up house prices and negating the average saving to heaping a heavy workload on time-pressured conveyancers.

“Property lawyers have been working around the clock to get people into their homes before the initial 31 March cut off. The conveyancing workload is unlikely to get any lighter given the holiday is now running until June and tapering through to September.

“In the long term, the industry needs to put conveyancing capacity – not to mention mental wellbeing – at the top of the agenda given the pressure law firms have been under to ensure clients complete on time. It is clear the traditional way of performing due diligence on transactions is getting in the way of efficiency, and we need to pivot quickly to digital, data-led solutions that can improve the experience for homebuyers and their advisers.”